“One homeless family was actually given the flat [for temporary accommodation] that they’d just been evicted from. They’d been long-term tenants in that flat. Their landlord evicted them, because he worked out he could get more money if he offered the flat to the council on a Nightly Lets basis. When the family turned up at the council as homeless after the eviction, the council offered them the same flat they’d just been evicted from – this time as temporary accommodation at a higher rent.”

This is the first in a series of articles I plan to publish based on interviews with a council homelessness officer I’m working with. This officer has worked in a number of different council housing offices in London and Greater London in the last 20 years and still works as a frontline council homelessness officer in and around London.

This officer interviews homeless people when they go to their local council for housing help, decides whether that council has a duty to house people who are homeless and must help find accommodation for people if a council does have a duty.

These days, this officer finds the job depressing and almost too difficult to contemplate. Antidepressants and sick days are features of this person’s life. Going without a job and the income isn’t possible, though.

The officer will remain anonymous in these articles.

—————————————————

First article:

Watching voracious landlords screw every pound they can out of homeless families and councils

This first article is about the problem that homelessness officers have finding temporary accommodation for homeless people who desperately need a place to stay that day.

In the interview transcript below, the officer talks about two major problems.

The first is nightly lets /nightly paid accommodation. The officer explains how money-hungry landlords make flats available to councils for homeless families on a night-by-night basis only, rather than for longer-term, more secure lets. The nightly lets options can be more lucrative for landlords. Landlords can also evict families more easily when a flat is let on a nightly basis.

“Nightly lets – you’re talking mostly about the crappiest accommodation in London, or outside of London,” the officer says.

The officer describes one case where a family who’d just been evicted from a flat they’d lived in for several years went to their local council for help – only to be placed straight back in the flat they’d been evicted from on the very same day, at a higher rent. The landlord had realised he could get more money by letting his flat on a nightly basis. He evicted the family and offered the flat back to the council as a nightly let for a higher charge:

Says the officer:

“There was a family that had been evicted from their house. They were [in] private rented. The landlord’s served a notice [to evict the family] – “[he’s said] oh, I want the property back.”

The family were evicted about 9’o’clock that morning. They came into [the] council.

The officers said, “we’ll give you temporary accommodation.” The accommodation that was given to them was the very house that they were evicted from that morning.

Basically, the landlord’s realised that he can get more money for this property as a nightly let. [He’s decided] “I’m going to evict these people.”

He’s obviously gone to the council and said, “here’s a property that’s going to be available on this day. You can have it as a nightly let.”

They went to that flat. Imagine how pissed off they were. They’d been packing all their stuff up for three weeks and put it in storage.

They’re like, “where are we going?” [The council is like] – it [your new temporary accommodation] is very close to where you were living before… and you’re going back there, with the same landlord who evicted you.” Continue reading

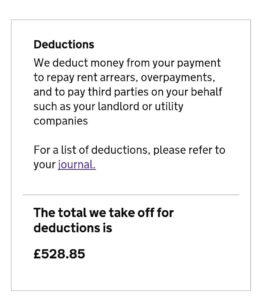

Getting very sick of

Getting very sick of  Another example of Universal Credit lunacy:

Another example of Universal Credit lunacy:{kind=link}