A few thoughts on Labour’s plans to cap credit card interest payments to ease card debt:

I feel that the debt troubles of a particular group of people are being sidelined in the recent flurry of mainstream news stories about debt (have written about this in detail in recent times)

We’re hearing a great deal in the mainstream about student loans and student debt, and about credit card and car payment debt – debt that particularly concerns the middle and voting classes, as people on twitter have observed.

We’re hearing a lot less about the debts that are crushing people who are most marginalised:

Examples of those debts and costs:

– The council tax debt and outrageous court costs that are added to debts when people are summonsed to court for council tax non-payment

– The bailiff costs that rise by tens and hundreds of pounds each time a bailiff hammers on a door to demand council tax and other debt repayments

– The impossible landlord demands for rent shortfall money when housing benefit or Universal Credit don’t cover escalating rents

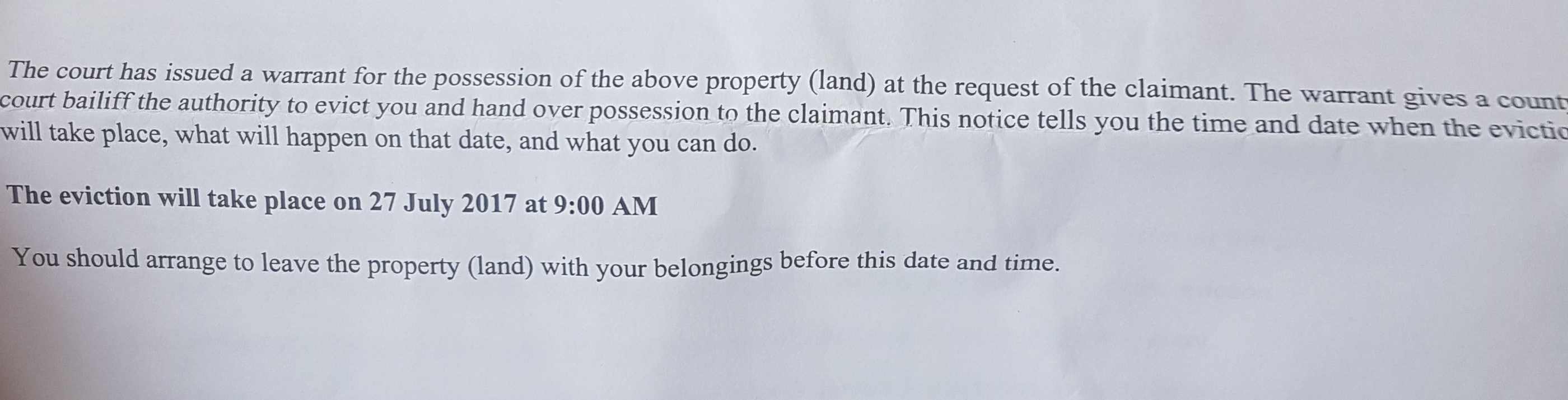

– The exorbitant court charges people must pay when eviction battles go to court (£355 for a woman on Income Support in this example).

– The DWP deductions from benefits for loans and advance payments that people must request to cover costs, Universal Credit start delays and all the rest.

– The sudden loss of income when Employment and Support Allowance recipients are found fit for work and told their ESA payments will stop.

Student loan debt and credit card debt are of course important topics. They’re not exclusive to the middle and/or voting classes. They just affect people who have a voice and use it. My point is that the crushing council tax demands, rent shortfall problems, benefit stops and delays, and court costs that keep the poorest people in debt are equally important. Payday loan regulation hardly addresses those problems.

If we’re going to talk about devastating debt which destroys lives, let’s include everyone in the discussion. Policy must be written for people who are the most marginalised, as well as people who are likely to vote. Such policy should be promoted and publicised as enthusiastically as any call for a card interest cap.

Throwing marginalised people a lifeline is not “being soft on welfare,” you know. It’s being humane – and fiscally responsible, I would have thought.

Regular readers will know

Regular readers will know

{kind=link}

{kind=link}