Getting very sick of Tory claims that Universal Credit advance payments solve the serious financial problems caused by the mandatory six weeks (it’s often longer) that people must wait for their first Universal Credit payment. This claim is a total fudge.

Getting very sick of Tory claims that Universal Credit advance payments solve the serious financial problems caused by the mandatory six weeks (it’s often longer) that people must wait for their first Universal Credit payment. This claim is a total fudge.

Let’s say this loud and clear: Universal Credit advance payments are LOANS. They must be repaid (you can read full details of the Universal Credit advance payment system on the CAB site). They’re not much-needed extras. They’re advances on people’s Universal Credit money and must be repaid out of people’s benefits.

That means that the DWP claws the money back when people’s Universal Credit claims are up and running. The DWP deducts advance payment loan money from people’s benefits at source. Those deductions mean that for months, people who were already in hardship (people who receive advance payments are in hardship by definition) get a smaller Universal Credit payment than they were expecting.

I’ve posted an example at the top of this article – an advance payment deduction notice from the Universal Credit journal of a Croydon/Colchester claimant I wrote about yesterday.

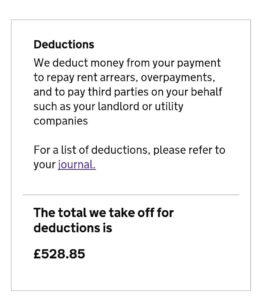

There’s another issue. The DWP makes mistakes with repayment totals – mistakes which cause people a great deal of stress and which they must try and sort out using Universal Credit’s unreliable online systems. For example: the woman who is paying back the advance payment in the notice above got a notice in her Universal Credit journal this year which said the DWP would deduct £528 that month. You can imagine how she felt when she saw that notice in her online account. She wasn’t even liable for payments listed in the notice:

When this sort of thing happens, people must spend ages on the phone to the DWP and online trying to sort the problem out – and trying to make sure, in this case, that the Universal Credit payment that month wasn’t £528 short. That deduction would have been a disaster. People who struggle to use online systems have no chance at all when these many mistakes happen. I’ve written in detail about problems JSA and Income Support claimants had and still have with DWP loan deductions. Some deductions put people in real hardship.

Let’s not forget either that often people who need advance Universal Credit payments already have other debts because of extra costs heaped on them by welfare reform – council tax debts and court costs, rent arrears and plenty more. The young woman in yesterday’s article had serious council tax and court debts, and tax credit repayment demands in the past two years. A deduction for a Universal Credit advance payment loan quickly becomes just another debt problem. Advance payments don’t solve problems caused by that six (and more) weeks that Universal Credit claimants must endure with no money.

All a Universal Credit advance payment does is push shortfall problems back for a short time – ie, until after Tory party conference is over and attention has moved from Universal Credit.

Does my head in, this. Just pay people their Universal Credit entitlement from the day they make their claim and be done with it. Any other so-called “fix” is garbage.

Another example of Universal Credit lunacy:

Another example of Universal Credit lunacy:

{kind=link}

{kind=link}